Subscribing to faith, part 2

Subscribing to faith, part 2

If members become donors, how does that change “church”?

It’s been almost a month, and stuff has happened, so let me recap what I think I was trying to say in part 1, https://open.substack.com/pub/knapsack/p/subscribing-to-faith

There’s an ongoing sea change in how people give to their congregations, and how the act of giving takes place, along with some connections between the act in worship and the discipline of personal stewardship. What I began with in part 1 was looking back over my own personal practice of financial management in general, stewardship on one hand, and pastoral care through guiding panicked people through fiscal meltdown on the other. Most of what I’ve done for myself and been able to do helping others is . . . not really working anymore. I mean, it could, such as writing down expenditures as a method of self-reflective personal management, but it’s all somewhat at odds with how people purchase items and spend money today.

Then we have the very specific set of issues around how people give to their church, their local congregation. I want to recap that part 1 survey of “old models” with the awareness of the fact that they come as a mix of these, with each congregation a different mix — while adding in one more before I get to my key question, one I’ll call the “endowment model” of local church support.

Loose offerings are what many people think of as “church offerings” but it has never been the bulk of any congregation’s income. How they are handled is a point of some dramatically different approaches in various churches: some places put all loose offering in the general fund, some all of it into missions or benevolences, while a few have a set percentage distribution for loose offerings. It’s a wild card, but as a percentage of total income usually rather low.

Pledged giving/offering envelopes is for most mainline Protestant churches the largest percentage of all giving. It’s usually set by a process in the fall before the new budget year, by initiative of the giver, and then the pledge is “fulfilled” through weekly, biweekly, monthly, or quarterly gifts, most often by check. Churches I’ve served over the last forty years saw three-fourths or more of their income from “the envelopes.”

Dues based giving is a model that many churches in my experience directly reject, but pastorally I have to note that as you talk to church folk you will find them perhaps using the church terms but their overall discussion of their giving is in the grammar of dues paying. “I missed my pledge last month when I was out sick, but I’m going to catch up,” or “Can I give you my pledge for next week, since I will be gone?” Again, church treasurers and board officers and clergy may very specifically say we aren’t operating on a dues basis like a club or social group, but that’s the mentality people often bring to their giving. And there are faith based organizations that embrace a dues model around membership. This grey zone is one reason many younger clergy reject the whole concept of “membership” as an element of church life, since it seems to feed the parallel idea of “dues paying” members.

The Tithe model has a very mixed history in the sort of mainline/oldline Protestant churches that I’m talking to for the most part. It has an implicit root system in a sort of Biblical literalism that most progressive Protestant bodies disavow generally, but when it comes to assumptions around giving tied to some sort of ten percent of the whole, it can suddenly sprout some very inerrant, text-tied expectations. More conservative and traditionalist Christian groups may use tithing as a simple, straightforward expectation for giving by leaders at minimum, if not for membership in good standing generally. Is the tithe after taxes, or on gross income? This debate can get into the weeds in a big hurry. However you calculate the ten percent, tithing has a Christian history which erupts in a variety of ways into ongoing church life and stewardship education, but most clergy will tell you tithers are a very small number of the total giving units. Some solid data gathered over the last few decades suggests 2.2% of total income as an average giving amount from regular givers in any US Protestant church.

Membership model giving is a term I don’t love, but I need to use something for an increasing occurrence in congregational stewardship: those who give a single annual gift to affirm their membership, often at year end, as you do for the American Legion or membership in the art museum, arboretum, symphony orchestra. It may be biannual; somewhere beyond the weekly to monthly pledged giving is the annual or a few times a year gift that is to me a different mindset around giving and membership. It’s where a person who sits down to write a series of once a year checks makes their church giving one more on that list; these can be substantial, and are important in the overall church budgeting and fiscal projection, but I would argue they represent a very different approach which requires something of a different form of cultivation.

What I wanted to add before moving on to where I see things going: the Endowment model. Here, too, I will be sloppy if only to prevent having a confusingly large number of categories. This is income to the local church which comes not from a person or family making a regular or annual decision, but the proceeds from endowed funds and I’m throwing in external income of all sorts. For various management reasons you need to sort these out differently, but here I’m just going to ask you to think about rent from a preschool on site, other building or facility use fees, and income from a trust account or investments as one big category. In general, your serious givers in a church know about the existence of endowment model income, and it factors into their thinking, which is where you need to be clear and honest about how that gets used, not the least because you may well want people to think about giving to build that endowment (or contribute to support upkeep or capital expenses that keep rental income arriving in your accounts). I’ve seen churches try very hard with good intentions (mostly) to hide their endowment income for fear it will reduce giving, and I’d say that’s a classic pennywise, pound foolish approach. Having said that, this sort of income to the general fund can be a substantial percentage of the whole, but it’s not taken as seriously as pledged giving, and I think that’s a mistake.

Special offerings also need to be added here; these are a very Disciples of Christ reality, but most church bodies have some form of them. How they pass through church fiscal reports can create some confusion, and some church treasurers are themselves confused about how they work. They also have long puzzled church leaders about how promoting giving that goes 100% outside of the local church affects giving; this is a parallel to the vexed question of how a capital campaign has an impact on general fund giving in any sort of organization. Without answering those questions, you do need to take them into account as we think about how giving influences how we think about and how we “do” church. It’s also an awkward reality that sometimes giving gets shifted to or between special offerings in order to make certain organizational points (such as stopping giving to DMF and moving that amount over to Week of Compassion).

There’s actually another model I’ve had pointed out to me in the month since I started working on this question, and that’s a Retail model of church income. “RETAIL model” you ask? Yep. There are local churches which operate their own businesses on the side which cover some or even a significant amount of the costs of their ministries. Coffee shops, restaurants, their own child care or preschool programs or even a charter school of their own (this is different from having HeadStart or some other separate day care paying rent to use the church building, which I put under the “Endowment model”).

To recap:

Loose offerings

Pledged giving/offering envelopes

Dues based

Tithe model

Membership model

Endowment model

Special offerings

Retail model

Those eight approaches all promote different assumptions and expectations around how the person giving in that way relates to the church. They also, I would argue, require differing approaches in how you manage and promote further giving under that model, and getting a “giving unit” in one approach to shift to another model has a variety of uphill and downhill effects. The most common in local church stewardship is thinking about how to encourage a pledged giver to become a tither, a definite “lift” or uphill push.

Congregational stewardship can in many settings be framed as the ongoing attempt to get loose offering people to move to offering envelopes and from there to tithing and possibly even into giving special gifts not only to special offerings but to the endowment of the church, usually in an estate gift or through required minimum distributions. There are all sorts of objections to this four stage model, but it is the mental map many church treasurers and perhaps far too many leaders in general, lay and clergy, use for thinking about stewardship.

Bruce Barkhauer with our “Faith & Giving” office reminded me after I posted part 1 of this of his office’s video summary of a few of these questions, which I am more than happy to commend to you all. It’s a little over seven minutes and well worth your time:

[Don’t worry, I’ll wait! Go ahead.]

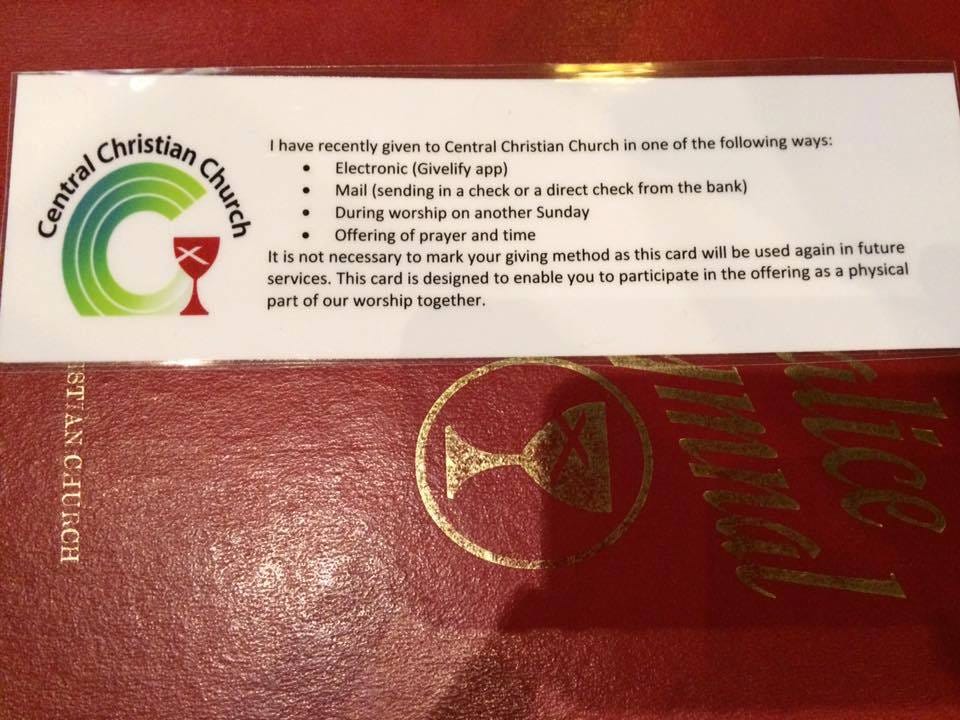

That’s more focused on the question of whether or not local churches should still have a “collected” offering as part of the worship service on Sunday. As Bruce gets at in the video, this was for a couple of generations the way 90% of church giving came in, and for some of us it’s quite disorienting to think about dispensing with a collection time in the service . . . even though the percentage of all giving received by many churches during worship itself has been dropping since before COVID. The changes in contact protocols and the challenges in having the personnel for passing around offering plates and such, all simply intensified existing trends: see the eight models I outline above.

Which finally brings me to: the Subscription model, often called in public non-profit circles the “sustaining gifts” approach, the “just $19 a month” model.

I don’t like it.

I don’t know if we can avoid it.

I don’t think it’s going to work out well for us to see it our core or primary mode of receiving offerings, but I’m not sure what our options are going to be.

[pause, deep breath]

=+=+=+=

In retail world, the subscription model is becoming the new gold standard. Why have someone make a purchase when you can get them to subscribe? Over time, you get more money than you’ll receive in a one-time payment for a good or service, and you support your own cash flow nicely in a very predictable fashion. And more importantly, you can potentially get people to pay you even when they aren’t calling on you for services rendered or anything delivered. Like gift cards that go unused, or aren’t redeemed in full, that’s pure profit.

At the end of part 1, I offered these two links as a quick overview of the developing “subscription economy.” Check them out now, if you wish:

https://www.axios.com/2023/11/24/membership-subscription-economy-business-model

https://www.nber.org/papers/w31547

This is the model streaming services are going to, of course; it’s also a major factor in non-profit fundraising, with the “arms of an angel” and sad puppies leading the charge some years back to convince folks to allow a charity access to your bank account and quietly, silently, enduringly get “just $19 a month” out of your pocket.

Should churches go down this road?

I am sure some reading this out there will say “we already are, and it works just fine, what’s your problem?” The quick answer, the short reply is “I don’t know what my problem is, and more power to you.” Getting automatic withdrawal from a church member for their monthly giving saves a step, especially as people don’t carry cash, and increasingly they don’t use or even have checks to write. If there’s no cash in pockets, if only the older members and a fraction of those at that are still writing checks, isn’t this the logical next stage of church giving?

Logical, yes. A good idea? I am nervously not so sure.

Granted, that non-denominational new plant contemporary worship church down the road a bit, the one in a big windowless box with a rockin’ praise team and forty minute sermons, a great children’s program and if you check the website, no women on the elder team? They never did a passed offering element in worship; they push hard for direct deposit automatic withdrawal electronic transfer from the get-go.

The large Catholic parish in your town? They generally don’t see a majority of their giving come through what is placed in baskets or donation boxes. They have seen much of their giving, which in many cases was annual, go to electronic fund transfers set up as new members fill out their parish transfer paperwork.

Synagogues or mosques? They’ve never had an offering element during worship itself for the most part.

So, I ask myself, what’s the problem? If churches which had passed offering plates for years are no longer doing that, isn’t it just another one of those transformations that take place every century or two in Christian life which often are forgotten once they occur, as each generation tends to think how things are done now are how they’ve always been?

Historically, the average person having “cash” was uncommon; in early America, which is where our roots in the Disciples of Christ are, cash money was unusual, barter more common. The early congregational histories have charming tales whose homeliness we might find obscuring some of the practical realities of those early generations: people building a church, for instance, with a list of contributions including “a bucket of nails” or “two bolts of woven cloth” along with “fifteen bushels of rye” and “seven basket loads of dried apples.” That’s all they had, then the elders had to figure out how to convert the goods and materials donated into the timbers and hardware of the church building they were working towards.

Even past the frontier period, those quaint tales of preachers being paid in produce: not a joke. That’s what they could give, and that’s what the minister received for their labor.

I mentioned the fascinating twist of learning in a church consultation about their posted lists in the 1920s of what each family gave, and how the stewardship campaign of those days overtly encouraged people to look at what their peers were giving on the bulletin board in the back of the church. For those of us conditioned by years of secrecy around who gives how much, that’s startling.

What that glimpse is telling us, I believe, is the rise of the money economy in the late 1800s, of stated wages becoming a norm in the early 1900s; where I suspect the change to non-disclosure comes is the rise of labor unions in the 1930s, and new tensions between workers and management, leading to a very intentional discretion about people knowing what each other made.

If you’re a farmer, it is still the case that people talk to each other about crop yield, field production on different parts of your land, and everyone tends to know who’s doing well and who isn’t. If you are a laborer in a paid position, the whole dynamic of raises and promotions, and the disjunction between union worker and middle management, makes open knowledge around who makes what a more awkward proposition — and as a church whose history has tended to be agrarian in origin, but which became much more a middle management, skilled labor social group, we slid into habits reflecting these tensions. Famously, we don’t tend to be the judges and principals and bosses: Disciples tend to be clerks and teachers and secretaries. There are exceptions, of course, but in the social stratification of middle America, the Episcopalians and Presbyterians tend to be the church of those “in charge” while the Baptists and Pentecostals tend to be the church of the strata our families are working to rise above. That’s rough, but I’d say accurate.

However you sort it out, we went pretty quickly in the rising cash and retail economy to a culture of confidentiality around giving, which has some kind of parallel to the workplace culture of confidentiality around compensation. Now we find ourselves moving into a cashless economy, and our assumptions and expectations are going to be adjusted again.

If you recall from my long intro in part 1 of this, I found “the envelopes” approach of managing my expenditures through putting set amounts of cash into designated envelopes, and doing the same thing for maintaining my giving, to be a very useful tool. It was one I often commended to others as a pastor when people were struggling with their own income versus expenses challenges. If you’d asked me thirty or twenty or even ten years ago, I think I would have said that’s always going to be a good tool for bringing some awareness, conscious spending, practical discipline into my fiscal life. It turns out that method was itself of a very particular period of time.

Which is where on a very granular level, I have my concerns, as to how I can myself, and from my own practice guide and advise others, in fiscal discipline. If the hard, practical, objective use of cash money in designated envelopes isn’t a realistic option, I have to look to new tools and methods.

Likewise, in the pastoral care issues I outlined in part 1 around helping people figure out where they stood, financially, and how to move forward. If our expenditures are becoming ever more frictionless, passive, invisible, up to and including our benevolences, church-wise or otherwise, how would I today help someone who is falling drastically behind figure out where and how and what to do about it? If I can no longer sort through envelopes with billing statements and arrearages, bank accounts and pay stubs, how would I help someone reconstruct their financial position who has come in because they’ve lost the thread themselves?

Well, I can only complain about it for so long; at some point, you just have to start working with what you have. If someone is into seven streaming services and is paperless in all their utilities and other obligations, delving back through the virtual threads of actual costs is going to have to become something different, something new.

But in trying to figure out how to advise and guide new clergy who are just starting to encounter the reality of a senior citizen member who is deep in a hole and can’t even tell you what their income and outgo is, I’ve also become concerned about the implications of all these shifts for giving and offerings and what is more and more being referred to openly as “donor management.”

Stay tuned for part 3, where I’ll try to bring all these strands together, and I hope in less than a month. What does it mean to “subscribe to faith”?

Closing: a worshiper in the cash economy struggling with a deep question of stewardship — how much of what I have in my pocket can I put in the plate?